India’s iron ore landscape is entering a decisive decade. Premium-driven auction volatility, greenfield stagnation, and concentrated political control across key ore states are reshaping domestic supply and opening new doors for global producers.

This playbook provides a structured analysis of market, policy, and stakeholder forces, giving strategy, regulatory, and commercial teams a single source of truth to plan 2026–2030.

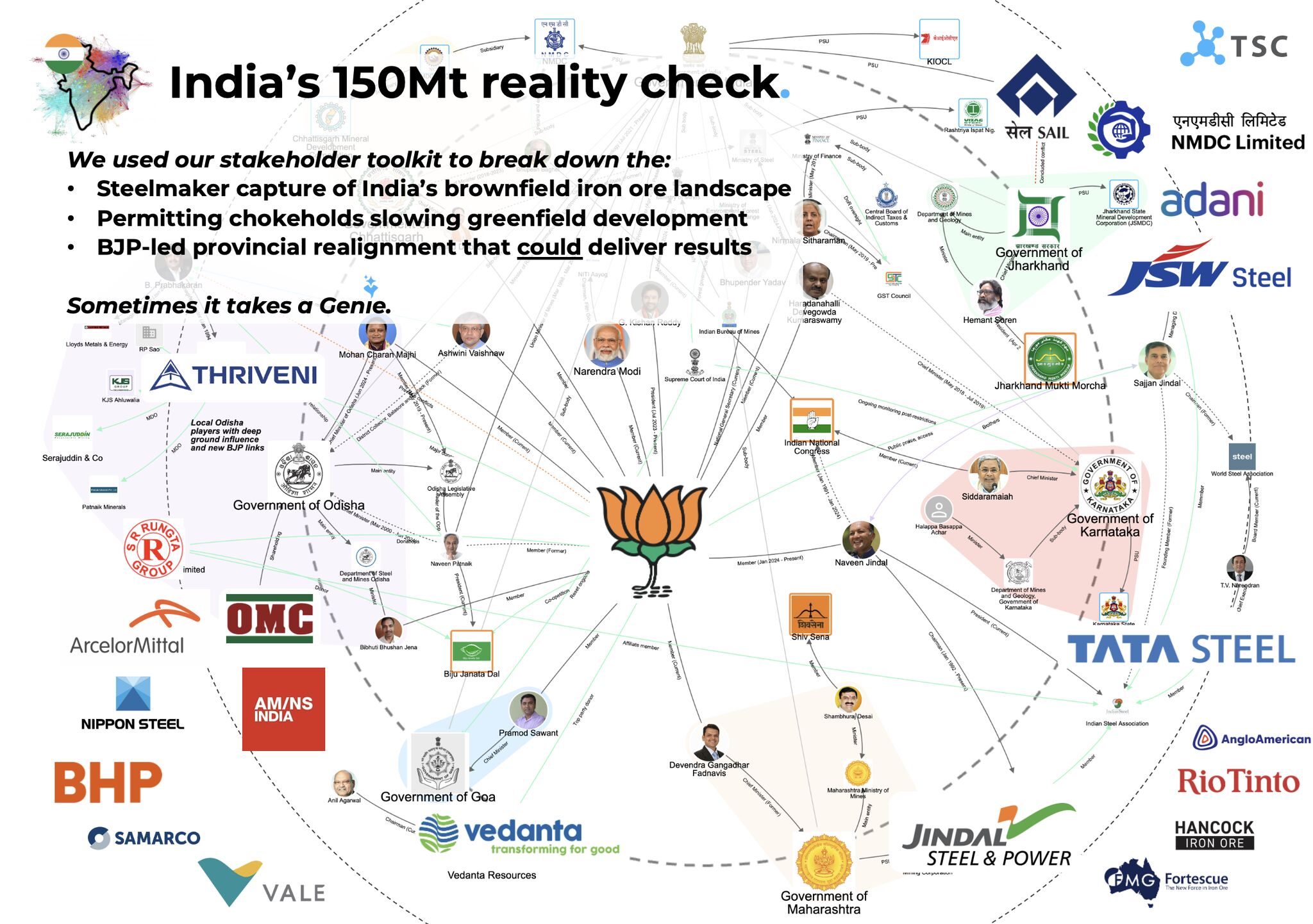

We mapped who owns what - and who holds sway. Here’s the snapshot:

1. Brownfield blocks: India’s biggest steelmakers (JSW Steel, AMNS India, Jindal Steel Ltd., Vedanta Group ) grabbed ~56 Mtpa or 60% of recent auction volumes. Instead of spurring development, premiums of +90-150% triggered lease surrenders, market volatility, and collapsing merchant discipline.

2. Greenfield blocks: Theoretically +42 Mtpa upside - if they get off the ground. Yet none auctioned post‑2020 has come online, and the handful due pre‑2030 are already burdened by the “winner’s curse.”

3. Politics: The Bhartiya Janta Party (BJP) now governs Odisha (2024) and Chhattisgarh (2023) - covering ~80% of India’s ore output. A premium‑system fix is being drafted, but state interests and local resistance will slow delivery.

A must-have for teams shaping decisions across mining, steel, trade, or public policy.

Download now.